60/30/10 Rule (or 60 30 10 Budget)

Using budget percentages to manage your money can simplify your financial life. The 60/30/10 rule budget advocates saving 60% of your income, then dividing the rest between needs and wants.

Saving and investing 60% of your budget could help you reach your dreams of retiring early and achieve financial independence. Those are the two central goals of the FIRE movement, something 39% of Americans say they’re interested in.

But is saving over half your income realistic? And how does the 60 30 10 rule budget compare to other budgeting methods?

Following a 60/30/10 budget isn’t necessarily right for everyone. But if you’re interested in how to apply this budget rule to your finances, here’s a closer look at how the 60 30 10 rule budget works and how it compares to other budgeting methods.

Related post: 30-30-30-10 Budget Explained (Pay Your Bills and Still Have Fun!)

LIKE FREE MONEY?

Here are some of my go-to apps for earning extra cash!

Survey Junkie. Earn up to $50 per survey just for sharing your opinions.

Swagbucks. Make money by playing games and watching videos. Join for free and get a $10 bonus when you sign up!

InboxDollars. Take surveys and get paid, no special skills or experience required!

Rakuten. Earn up to 40% cash back at hundreds of retailers, online or in stores. And get $30 for each person you refer, along with a $10 sign up bonus!

CashApp. Need a simple app for sending and receiving money? Get $5 free when you use code ‘VZXRXZN’ to join CashApp.

What Is the 60/30/10 Rule Budget?

In simple terms, the 60/30/10 rule is a budgeting method that’s based on percentages. Specifically, you’re budgeting money into three categories:

- Saving/investing

- Needs

- Wants

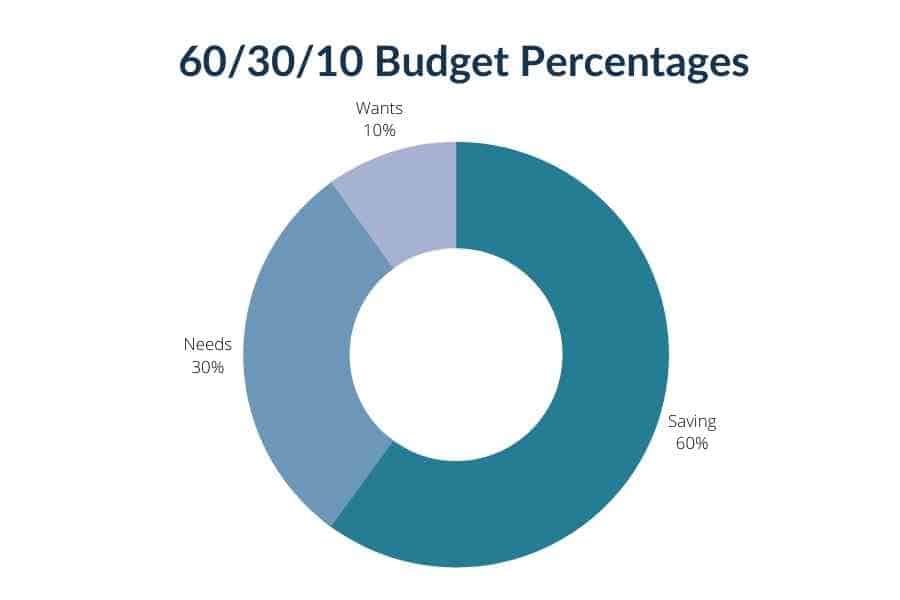

The 60 30 10 budget gets its name because those are the percentages you’re using to budget.

So, going back to the three budget categories listed above, the 60/30/10 budget breaks down like this:

- 60% of your take-home income goes to saving and investing to further your financial goals

- 30% of your take-home income goes to your needs — things like housing, utilities, food, transportation and health care

- 10% of your take-home income goes to discretionary spending or wants — this can mean things recreation, entertainment, new clothes or travel

Compared to other budget rules that use percentages, the 60/30/10 budget is pretty ambitious when it comes to saving.

Related post: 10 Good Money Habits That Can Make You Rich

Is the 60 30 10 rule budget realistic?

That’s a legitimate question. Because really, not everyone could afford to save that much of their pay each month.

For example, fewer than 4 in 10 Americans could pay for a surprise $1,000 expense in cash. Sixty-three percent of Americans live paycheck to paycheck.

If you’re struggling financially, then a different budgeting method could work better.

But if you have the means (and the resolve) to save 60% of your income, the 60/30/10 budget rule could put you solidly on the path to building wealth.

For instance, I save around 50% of my income now after handing over a chunk to the government for taxes. But I’m able to do that because of three things:

- I have no debt, other than my mortgage

- I’ve worked on growing my income

- I’m able to keep my expenses at 25% of my monthly earnings

It took years of hard work to get to this point though. So that’s something to keep in mind if you’re considering the 60 30 10 rule budget.

Related post: Why Is Budgeting Important?

Why budget by percentages?

You might be wondering why anyone would use a percentage budget rule anyway.

A lot of people like budgeting by percentages because it can simplify making a budget.

Compared to something like zero-based budgeting, which requires you to assign every single dollar a specific job, following a percentages budget rule can be easier.

When you budget by percentages, you’re just splitting your income into different categories. Then you assign each category a certain percentage of your income.

For example, with Dave Ramsey budget percentages you divide income across 11 budget categories. There’s also the 70 20 10 budget method and the 50 30 20 budget rule.

Some percentage budget rules use more categories; others use less. For 60 30 10 budgeting, you’re using just three.

All in all, it’s a low-stress way to budget and manage your money.

Related post: How to Teach Budgeting to Kids

How the 60 30 10 Rule Budget Works

Making a budget using the 60 30 10 rule for budgeting isn’t complicated at all. It’s a simple process that involves:

- Adding up all of your income

- Adding up what you plan to spend or save for the month

- Dividing spending and saving into the appropriate category

If you’re still confused about how to make a 60/30/10 budget here’s how to do it, step-by-step.

Start with your income

Income for the 60/30/10 rule budget means your take-home or after-tax pay. So this can include:

- Paychecks from your job

- Side hustle income

- Business or freelancing income

- Child support or alimony you receive

- Cashback earned from apps like Rakuten or Ibotta

- Refunds and stimulus checks

- Rebates

Basically, any money you receive for the month goes into the income pot.

60% of your take-home pay to saving and investing

With the 60 30 10 rule investing and saving are really the stars. Most of your money is going to this category each month.

If you’ve already added up your income, multiply that amount by 60% or 0.60. This will tell you how much to save or invest.

So, say you take home $5,000 a month. Here’s what the math looks like:

$5,000 x 0.60 = $3,000

In other words, you’re going to save or invest $3,000 of what you make. That’s $36,000 a year so it’s definitely not chump change.

But now you have to think about how you’re going to split that $3,000 up. This is where it helps to be clear about your financial goals.

For example, say you want to save for emergencies, put money into an IRA for retirement and open a college savings plan for your child.

You might save:

- $1,000/month in a high yield savings account

- $500/month in an IRA

- $1,000/month in a 529 college savings account

That would leave you with $500 left over.

You could add this money to sinking funds accounts to cover expenses you only pay once or a few times a year.

And if you want to buy a home, you might set up a down payment fund for that extra $500.

Or you could invest it in a taxable brokerage account instead. You can open an investment account with just $100 at M1 Finance.

The most important thing is to have a plan for all the money you’re saving. Otherwise you might be tempted to spend it instead.

Related post: Cash Envelope System for Beginners (Get Started in 3 Easy Steps)

30% of your take-home pay for needs

The next part of the 60/30/10 rule budget allocates 30% of your take-home pay for needs.

Needs include any expenses you have to pay to maintain a basic standard of living. That can include:

- Housing (i.e. rent or a mortgage)

- Utilities

- Transportation

- Groceries

- Insurance (i.e. health insurance, car insurance, etc.)

- Health care expenses

- Basic clothing

Anything that has to be paid each month would go into this category.

You could technically include debt repayment here. Though if you’re saving 60% of your income each month, it’s possible that you don’t have any debt at all.

Other essential expenses might include child care or expenses you need to pay to work from home. And if you’re obligated to pay child support or alimony, those payments would go here as well.

10% of your take-home pay on wants

The last part of the 60/30/10 rule budget is your “fun” money.

You get to spend 10% of your take-home pay on any wants. So that can include:

- Entertainment

- Dining out

- Travel

- Hobbies

- Recreation

- Salon or spa visits

Basically, anything you don’t necessarily need to spend money on would go into the wants category.

60/30/10 rule budget calculator

I searched high and low on the internet to try and find a 60 30 10 rule budget calculator that would let you plug in the numbers.

Since this is a less common budgeting method, I couldn’t find one. (And if you have, shoot me the link and I’ll include it!)

But it’s fairly easy to calculate budget percentages using the calculator on your phone.

First, figure out your total take-home pay for the month. Again, this is the money you get to keep after taxes and other employer deductions are taken out.

Then, to figure up 60/30/10 rule budget percentages you’ll need to do three simple calculations:

- Take-home pay amount x 0.60 = Amount to savings

- Take-home pay x 0.30 = Amount to needs

- Take-home pay x 0.10 = Amount to wants

That’s all there is to it.

If your income stays the same month to month, you’ll only need to do this calculation once.

But if your income fluctuates month to month, you’ll need to do the calculations again at the beginning of each new budgeting period.

60/30/10 Rule Budget Example

Having an example to follow makes it easier to see the 60 30 10 rule budget in action.

So, here’s what it looks like again if you make $5,000 a month:

- $5,000 x 0.60 = $3,000 to savings

- $5,000 x 0.30 = $1,500 to needs

- $5,000 x 0.10 = $500 to wants

And here’s how the 60/30/10 rule budget works if you make $10,000 a month:

- $10,000 x 0.60 = $6,000 to savings

- $10,000 x 0.30 = $3,000 to needs

- $10,000 x 0.10 = $1,000 to wants

I used rounded dollar amounts here for simplicity’s sake. But you can apply the same math to any monthly income to figure out how much to budget for savings, needs and wants.

And in case you need a monthly budget template to follow, you can download a free one here!

Other Ways to Budget by Percentages

As mentioned, the 60/30/10 rule budget isn’t the only way to divide up your income each month.

If you’re interested in other ways to budget, here are three options you might consider.

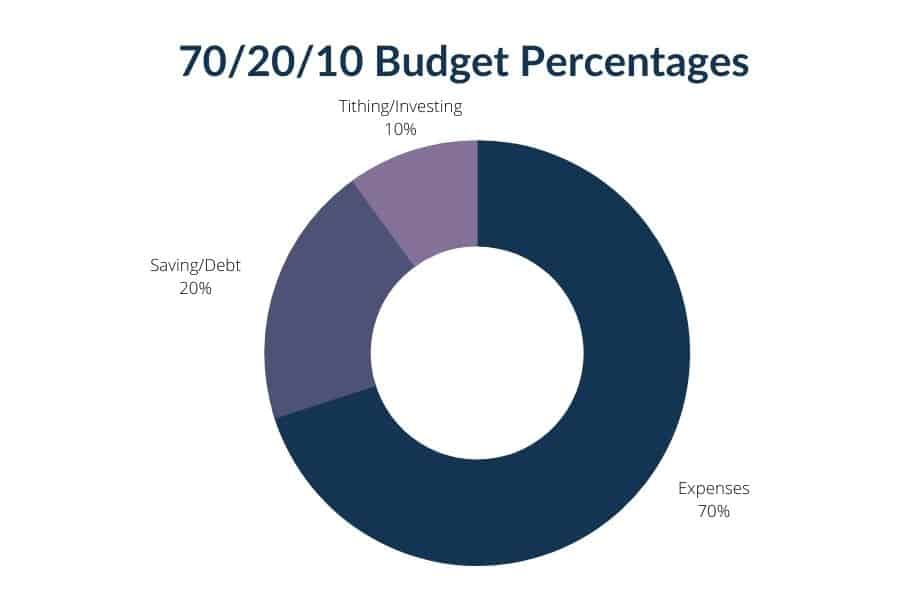

70/20/10 budget method

The 70 20 10 budget rule can be interpreted in a couple of ways. But generally, here’s how it breaks down:

- 70% of your take-home pay goes to expenses (this includes needs and wants)

- 20% of your take-home pay goes to saving (and/or debt repayment)

- 10% of your take-home pay goes to investing and/or charitable giving

I like the 70/20/10 budget rule for money because it specifically includes a percentage for investing.

Saving money is good but investing it is even better if you want to build wealth. When you invest, you can grow your money faster through compounding interest.

(And if you’re not investing yet, you can get started with as little as $100 at M1 Finance.)

This budget rule does lump all of your expenses together into a single bucket. So if you prefer to keep needs and wants separate in your budget, this one may not work for you.

Read my in-depth guide to how to use the 70 20 10 budget method here.

50 30 20 budget method

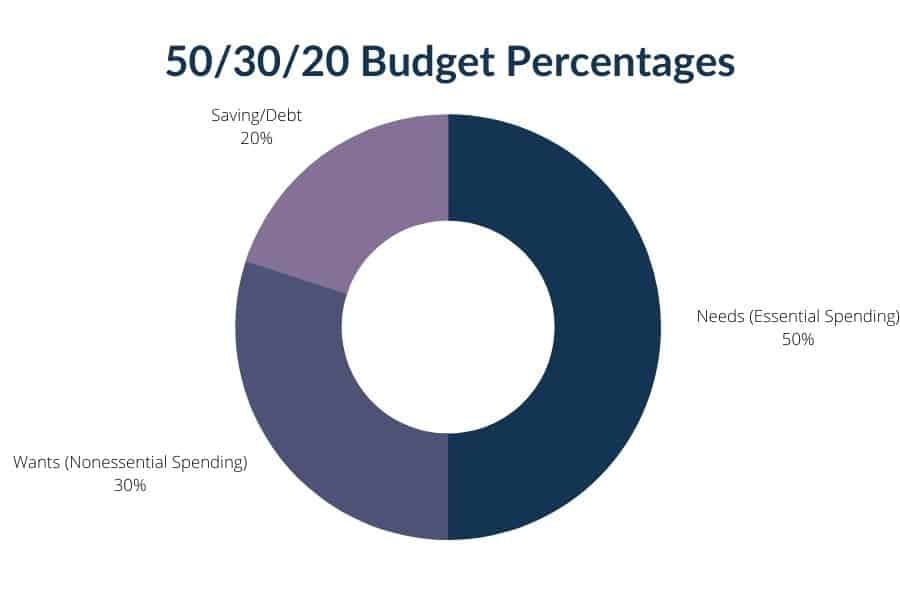

The 50/30/20 rule for money was developed by Senator Elizabeth Warren (D-Mass.) in her book, “All Your Worth: The Lifetime Money Plan.”

Her budget system breaks down spending like this:

- 50% of your take-home pay for essential expenses (needs)

- 30% of your take-home pay to discretionary expenses (wants)

- 20% of your take-home pay to savings and debt repayment

Out of all the different ways to budget using percentages, the 50-30-20 rule is the one I see talked about the most.

I’m not sure if that’s because it’s truly the most popular budget method or if it’s because of Senator Warren’s name being attached to it. At any rate, this one is good if you like to keep needs and wants separate.

There’s no special category for investing; that gets included with savings. And if you have debt to pay off, you might not be able to save 20% of your income using this budget method.

Here’s a detailed guide to how to make a 50 30 20 budget.

60 20 20 budget rule

The 60 20 20 budget rule offers another take on budget percentages.

With this method, your budget looks like this:

- 60% of your take-home pay goes to living expenses (i.e. housing, food, utilities, transportation, etc.)

- 20% of your take-home pay goes to financial goals (like paying own debt, saving and investing)

- 20% of your take-home pay goes to discretionary expenses

This method really isn’t that different from 70/20/10 budgeting or the 50/30/20 budget rule. You’re just dividing up your percentages in a different way.

This budget rule could be a good choice if you want to allocate less of your money to discretionary spending.

If your basic living expenses take up a big chunk of your paychecks, for example, the 60/20/20 rule budget could work for you.

What is the Best Budget Rule?

In simple terms, the best budget rule is the one that works for you.

It’s the budget rule that fits your income, spending habits and money goals.

For some people, that might be the 60 30 10 rule budget. For others, it might be 50/30/20 budgeting or Dave Ramsey budget percentages.

The great thing about budgeting is that you don’t have to get it right the first time.

You can experiment with different budgeting methods to find the best one for you. And you might find that the best budget rule for your 30s isn’t the one you use in your 40s or 50s.

Bottom line? Life changes and your budgeting system might need to change and adapt as well.

The important thing is that you don’t give up on the concept of budgeting.

Final thoughts on the 60/30/10 rule budget

The 60 30 10 rule budget is designed for super savers.

If you have fairly low living expenses, low or no debt and you don’t spend much on wants, then this budgeting system could work for you. Saving 60% of your income could be huge if you want to retire in your 40s instead of waiting until your 60s.

The 60/30/10 rule budget does take discipline to stick to. And you’ll need to be smart about drastically cutting your expenses.

But if you can make it work for you, it can pay dividends when it comes to building wealth.

Have you tried the 60 30 10 budget rule? How did it work for you?

Head to the comments and tell me about it, then be sure to share this post.

And don’t leave without your free printable budget and saving templates!